This article is sponsored by Agents for Impact (AFI). We invite you to learn more about the firm via LinkedIn.

Andrij Fetsun, Founder & CEO at AFI:

Andrij Fetsun, Founder & CEO at AFI:

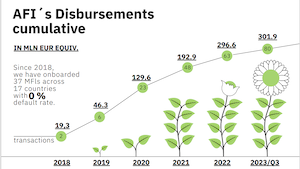

AFI celebrated five years in business in October this year, and my team has attained several impactful goals during this challenging time. This would not have been possible without the immense support of our clients: the German impact-driven microfinance fund Invest in Visions, which has accumulated a volume of around EUR 1 billion with a major focus on microfinance; HANSAINVEST, which is based in Hamburg; and the crowdfunding platform Lendahand. Among the services we provide these clients is to perform plausibility checks of their funds’ ESG reports.

As the founder of AFI, I would like to highlight the culture we have built with our dedicated team that has come together during these five years from different parts of the world. I believe that corporate culture is crucial for every company, especially for startups. Initially, we had trouble attracting Agents since we were not a well-established name in the industry or able to pay high salaries from the outset. Therefore, I focused on what truly makes for a great workplace

As the founder of AFI, I would like to highlight the culture we have built with our dedicated team that has come together during these five years from different parts of the world. I believe that corporate culture is crucial for every company, especially for startups. Initially, we had trouble attracting Agents since we were not a well-established name in the industry or able to pay high salaries from the outset. Therefore, I focused on what truly makes for a great workplace

Diana Chepng’eno: Sitting within the UN Environment Programme Finance Initiative, under the Principles for Sustainable Insurance, we are ramping up a Sustainable Insurance Facility. We launched the facility in 2022 to advocate for the importance of insurance for micro-, small and medium-sized enterprises (MSMEs) in V20 countries as a significant driver for mitigating climate change risks. MSMEs, for example, comprise about 75 percent of the total GDP of the V20. Therefore, if we can support these MSMEs by facilitating access to much-needed insurance, so that they may become more climate resilient, then these entire countries can be climate-resilient.

Diana Chepng’eno: Sitting within the UN Environment Programme Finance Initiative, under the Principles for Sustainable Insurance, we are ramping up a Sustainable Insurance Facility. We launched the facility in 2022 to advocate for the importance of insurance for micro-, small and medium-sized enterprises (MSMEs) in V20 countries as a significant driver for mitigating climate change risks. MSMEs, for example, comprise about 75 percent of the total GDP of the V20. Therefore, if we can support these MSMEs by facilitating access to much-needed insurance, so that they may become more climate resilient, then these entire countries can be climate-resilient. This forum will bring stakeholders together to discuss topics such as: (1) Climate-smart Financing for Smallholder Farmers; (2) Women’s Economic Empowerment by MFIs [Microfinance Institutions]; and (3) Green & Sustainable Finance; Genuine Change from MFIs.

This forum will bring stakeholders together to discuss topics such as: (1) Climate-smart Financing for Smallholder Farmers; (2) Women’s Economic Empowerment by MFIs [Microfinance Institutions]; and (3) Green & Sustainable Finance; Genuine Change from MFIs.